Marion County is preparing for the possibility of drastically reduced budgets for emergency services and other departments as voters decide the fate of an upcoming property tax amendment this November, with projections showing the county could lose over $50 million of its tax revenue in just the first year alone.

In anticipation of the possible changes coming later this year, the Marion County Board of County Commissioners will host a workshop on Monday, July 13, at 9:00 a.m. at the McPherson Governmental Campus Auditorium. The meeting will focus entirely on discussing the state’s joint resolution regarding property taxes and its looming impact on the county’s financial future.

In a 24-page workshop presentation, the county details the projected fallout from House Joint Resolution 1F (Amendment 3), a measure focused on homestead property exemption reform.

If approved by voters, Amendment 3 would replace the current non-school portion of property tax exemptions with a $150,000 exemption starting in January 2027. That exemption would then increase to $250,000 in January 2028. Additionally, the amendment would cap assessment increases on non-homesteaded properties to just 5% over the prior year.

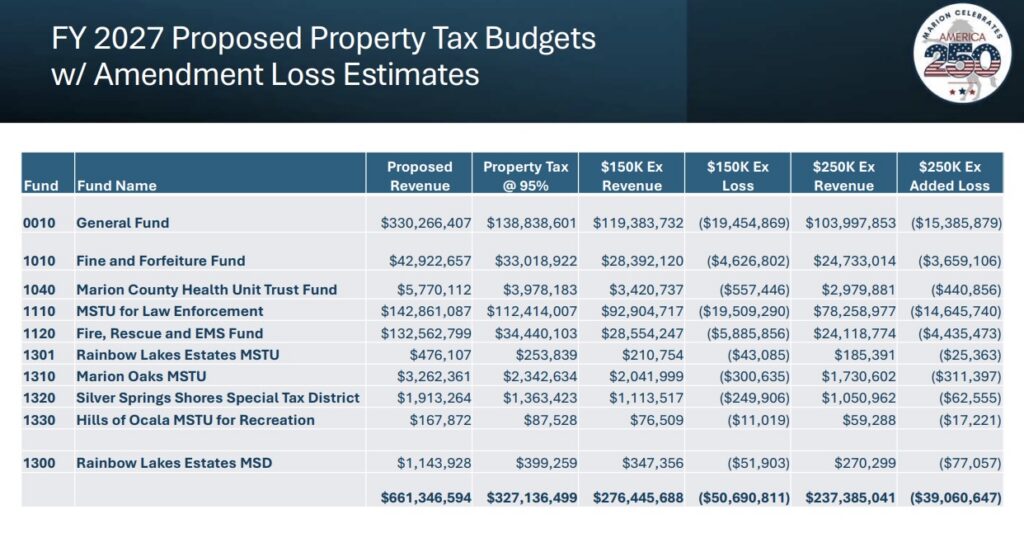

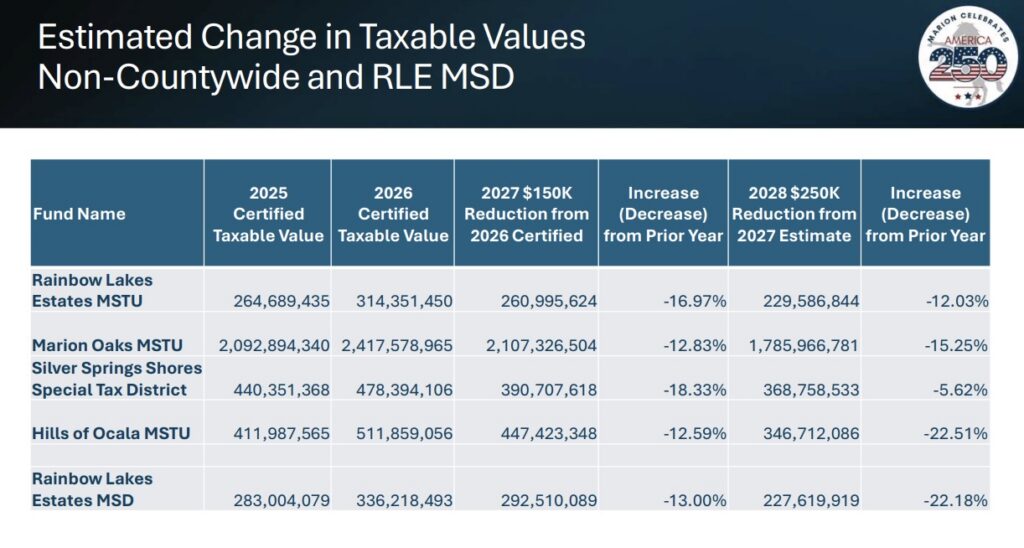

According to the county’s taxable value estimates, the implementation of the $150,000 exemption in 2027 would trigger a 14.01% decrease across several major county funds, including the General Fund, Fine and Forfeiture Fund, County Transportation Maintenance Fund, and the Health Unit Trust Fund.

When the exemption climbs to $250,000 the following year, those same funds would experience an additional 12.89% drop.

Other critical public safety funds would be hit even harder.

The municipal services taxing unit (MSTU) for law enforcement is projected to see a 17.35% decrease in 2027, while the fire, rescue and emergency medical services funds are bracing for a 17.09% drop.

In total, the county estimates a staggering revenue loss of nearly $50.7 million in the first year under the $150,000 exemption. The losses would compound by an additional $39 million when the exemption jumps to $250,000.

Furthermore, the amendment strictly dictates how local governments can spend their remaining ad valorem taxes. Revenues would be restricted to core services, such as providing for public safety, funding education, financing infrastructure and natural resource projects, and meeting local employee retirement benefits.

To bridge the funding shortfalls, the presentation warns that the county may be forced to drastically increase millage rates.

Projections show the General Fund millage rate could climb from 3.49 in 2027 to 4.66 by 2029, and the Law Enforcement MSTU millage could skyrocket from 3.72 to 5.35 over the same timeframe.

The Board of County Commissioners will dive deeper into these figures, as well as the potential impacts of Amendment 1 (Tangible Agriculture Property Exemption), during Monday’s workshop.

What are your thoughts on the topic? Share them in a comment below or, if you have more to say on the topic, write a letter to the editor.